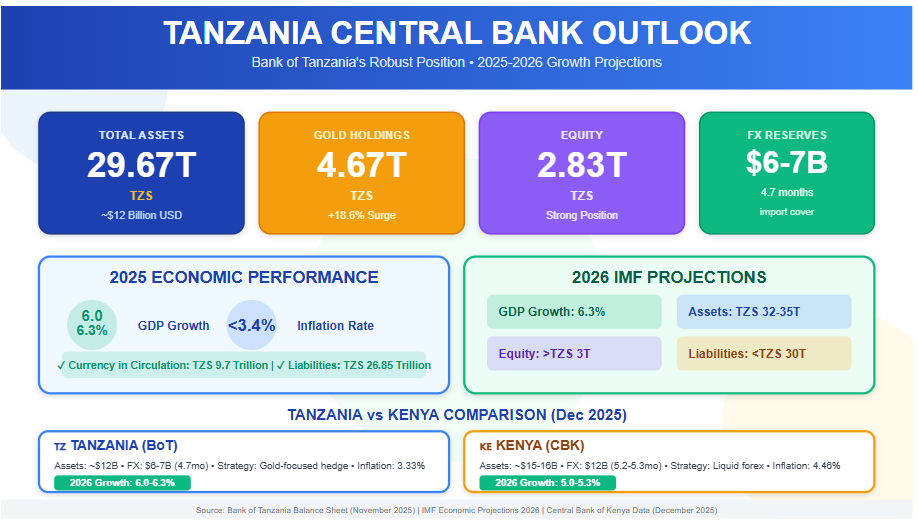

As of November 2025, the Bank of Tanzania (BoT) recorded total assets of TZS 29.67 trillion (approximately USD 12 billion), liabilities of TZS 26.85 trillion, and equity of TZS 2.83 trillion, featuring a remarkable increase in gold holdings (over TZS 4.67 trillion combined) and cash equivalents (TZS 4.45 trillion) driven by record gold sales and tourism revenue—this directly reflects Tanzania's strong economic performance in 2025, with GDP growth of 6.0–6.3%, inflation below 3.4%, and foreign exchange reserves of USD 6–7 billion (4.7 months of import cover). The BoT plays a critical role in managing the economy through monetary policies, such as purchasing domestic gold, controlling currency in circulation (TZS 9.7 trillion), and extending loans to the private sector to stimulate investment and sustainable development.

If this trend continues into 2026, in line with IMF projections (GDP growth of 6.3%), BoT assets are expected to reach TZS 32–35 trillion, liabilities to remain well-managed below TZS 30 trillion, and equity to strengthen above TZS 3 trillion—signaling a steadily growing and resilient economy. In comparison, the Central Bank of Kenya (CBK) holds total assets of approximately KES 2 trillion (USD 15–16 billion) with foreign reserves of around USD 12 billion (5.2–5.3 months of import cover) as of December 2025; while the CBK offers stronger liquid foreign reserves for greater protection against shocks, the BoT's gold-focused strategy provides a hedge against global price volatility, with both institutions contributing to their countries' growth (Kenya projected at 5.0–5.3% in 2026) through effective inflation control and credit stimulation. Read More: Central Bank Asset Dynamics and Tanzania’s Macroeconomic Performance in 2025–2026

In East Africa, the Bank of Tanzania (BoT) and the Central Bank of Kenya (CBK) stand as critical institutions steering their respective economies toward stability and expansion. As of December 2025, both nations exhibit resilient growth trajectories, with Tanzania's GDP expanding by 5.6% in FY2024/25 and projections for 6.0-6.3% in 2025-2026, while Kenya anticipates 5.3% growth in 2025 amid controlled inflation. These figures reflect the central banks' pivotal roles in fostering economic development through monetary policy, reserve management, and financial stability. However, Tanzania's post-election political turmoil in late 2025 introduces risks that could dampen its 2026 outlook, underscoring the interplay between governance and economic progress. This article examines the functions of BoT and CBK in driving growth, offers a comparative lens, and explores how Tanzania's political dynamics might influence its economic path forward.

The BoT, established under the Bank of Tanzania Act of 2006, serves as the guardian of monetary stability while actively supporting broader economic growth. Its primary mandate includes formulating and implementing monetary policy to maintain low inflation—currently at 3.33% in 2025—and ensuring financial system soundness. Beyond price stability, the BoT contributes to development by developing financial markets, promoting inclusive finance, and accumulating foreign reserves to buffer against external shocks. For instance, its November 2025 balance sheet reveals total assets of TZS 29.67 trillion (approximately USD 12 billion), bolstered by an 18.6% surge in gold holdings to TZS 4.67 trillion, reflecting strategic purchases from domestic miners to diversify reserves and support the mining sector—a key driver of Tanzania's export-led growth.

By managing currency in circulation (TZS 9.7 trillion as of November) and extending loans to the private sector (up 62% month-on-month to TZS 1.35 trillion), the BoT stimulates investment in agriculture, tourism, and manufacturing, which employ over 65% of the workforce. In January 2025's Monthly Economic Review, the BoT emphasized aligning monetary policy with growth objectives, such as sustaining reserves at USD 6.17 billion (4.7 months of import cover) to enhance investor confidence and facilitate infrastructure projects like LNG developments. These efforts have helped Tanzania achieve resilient GDP growth despite global headwinds, positioning the bank as a catalyst for long-term development through policies that encourage savings, credit access, and economic diversification.

Similarly, the CBK, mandated by Article 231 of Kenya's Constitution, prioritizes price stability while promoting economic growth and public interest. It formulates monetary policy, issues currency, and regulates the financial sector to foster a stable environment for investment. As of December 2025, the CBK lowered its Central Bank Rate (CBR) to 9.00% from previous levels, aiming to stimulate economic activity, support SMEs, and boost lending amid inflation of 4.46% in November—well within its 2.5-7.5% target. This proactive stance, as outlined in its bi-annual Monetary Policy Statements, regulates money supply growth in line with GDP targets, using tools like Open Market Operations and a Cash Reserve Ratio of 3.25% to manage liquidity.

The CBK's foreign exchange reserves stand at approximately USD 12 billion (5.2-5.3 months of import cover), providing a stronger buffer than Tanzania's and enabling interventions to stabilize the Kenyan Shilling. By encouraging long-term investments and maintaining deflation-free conditions, the bank supports key sectors like agriculture, services, and manufacturing, which have driven Kenya's consistent GDP expansion. For example, its role in currency issuance and management ensures efficient transactions, while financial inclusion initiatives have expanded access to credit, contributing to poverty reduction and job creation. Overall, the CBK acts as an economic enabler, balancing stability with growth to position Kenya as a regional hub.

While both central banks share core functions like inflation control and reserve management, their approaches reflect national economic structures. Tanzania's BoT emphasizes commodity diversification, with gold comprising a significant portion of reserves, aligning with its mining-dependent economy. In contrast, Kenya's CBK relies more on liquid foreign currency holdings, suiting its service-oriented market with higher external trade volumes.

| Aspect | Bank of Tanzania (BoT) | Central Bank of Kenya (CBK) |

| Total Assets (est. Dec 2025) | ~USD 12 billion (TZS 29.67 trillion, Nov data) | ~USD 15-16 billion (KES ~2 trillion est.) |

| FX Reserves | ~USD 6-7 billion (4.7 months import cover) | ~USD 12 billion (5.2-5.3 months cover) |

| Key Growth Focus | Gold purchases, private sector lending; supports mining/tourism | Rate cuts for SMEs; stabilizes services/manufacturing |

| Inflation (2025) | 3.33% | 4.46% (Nov) |

| Policy Tools | Domestic gold acquisition, monetary easing | CBR at 9%, Open Market Operations |

| GDP Contribution | Enables 6%+ growth via reserves buildup | Sustains 5%+ growth through liquidity |

This table highlights Kenya's edge in reserve depth for external resilience, while Tanzania's strategy hedges against volatility through gold. Both institutions have effectively contained inflation below 5%, fostering environments conducive to investment and poverty alleviation.

Tanzania's political stability, once a regional benchmark, has been shaken by the October 2025 general elections, marred by allegations of irregularities and resulting in widespread protests. President Samia Suluhu Hassan secured re-election, but opposition parties like Chadema have decried the process as fraudulent, calling for a UN-overseen transitional government. Post-election violence led to a lethal crackdown by security forces, with UN experts condemning systematic human rights violations, including killings and digital restrictions. By December 2025, the government imposed nationwide protest bans, tightened security, and urged the military to remain apolitical amid escalating tensions.

This unrest could jeopardize Tanzania's 2026 economic projections of 6.1-6.3% GDP growth. Prolonged instability might deter foreign investment, disrupt tourism (a key forex earner), and strain fiscal resources through heightened security spending. If protests escalate, supply chain disruptions could inflate food prices, pushing inflation above the 3-5% target and eroding purchasing power. Moreover, international scrutiny from bodies like the UN and African Union could lead to sanctions or reduced aid, impacting reserves and infrastructure projects. However, if the government addresses grievances through dialogue—as hinted in recent calls for military professionalism—stability could return, allowing the BoT's policies to sustain growth amid global trade tensions.

The BoT and CBK exemplify how central banks can drive economic development by balancing stability with proactive growth measures, from reserve diversification in Tanzania to rate adjustments in Kenya. Their efforts have positioned both nations for robust 2025-2026 performance, with low inflation and adequate buffers against external risks. Yet, Tanzania's political volatility post-2025 elections poses a wildcard, potentially hindering 2026 growth through investor flight and fiscal strain. For sustained progress, addressing governance issues will be as crucial as monetary policy, ensuring these East African powerhouses continue their upward trajectories.

The Tanzania Shilling achieved a dramatic turnaround in June 2025, strengthening to TZS 2,631.56 per USD from TZS 2,698.42 in May, marking a remarkable shift from chronic depreciation to currency appreciation. This performance represented a stunning reversal of fortunes, with the annual depreciation rate plummeting from a concerning 12.5% in June 2024 to just 0.21% in June 2025—a 60-fold improvement that positioned the shilling among the best-performing African currencies. The stabilization was underpinned by robust seasonal foreign exchange inflows, including gold exports worth USD 3.66 billion and tourism receipts of USD 3.83 billion from 2.2 million visitors, while enhanced interbank foreign exchange market liquidity saw turnover increase to USD 121.50 million in June from USD 110.8 million in May. Critically, the Bank of Tanzania's intervention needs dropped dramatically to just USD 6.3 million in net sales compared to USD 53 million in May, demonstrating market-driven stability that coincided with inflation remaining controlled at 3.3%—well within the 3-5% target range—despite food price pressures, as the stronger currency helped offset imported inflation and contributed to energy inflation declining from 6.1% to 2.1%.

In June 2025, the Tanzania Shilling (TZS) demonstrated remarkable resilience, strengthening significantly against major currencies with the exchange rate averaging TZS 2,631.56 per USD, representing a substantial improvement from TZS 2,698.42 in May 2025. This performance marked a dramatic turnaround, with the annual depreciation rate plummeting to just 0.21% from 3.82% in May and a concerning 12.5% in June 2024. Recent data indicates the shilling's continued strength, with the USD/TZS exchange rate falling to 2,470.0000 on August 7, 2025, and the Tanzania Shilling strengthening 6.44% over the past month.

Key Drivers of Currency Stabilization:

A. Seasonal Foreign Exchange Inflows:

B. Enhanced Interbank Foreign Exchange Market (IFEM) Liquidity:

C. Robust External Sector Performance:

Inflation Trends:

Marginal Inflation Increase: Headline inflation rose slightly to 3.2% in February 2025, up from 3% in the corresponding period in 2024, with June 2025 recording 3.3% compared to 3.2% in May. The increase was primarily attributed to:

Mitigating Currency Effects:

Central Bank Policy Stance:

External Reserves and Liquidity:

GDP Growth Trajectory:

Export Performance:

Positive Stability Indicators:

A. Price and Monetary Stability:

B. External Sector Resilience:

C. Financial Sector Development:

Growth Support Mechanisms:

| Factor | Impact on TZS Stability | Link to Inflation | Economic Growth Effect |

| Seasonal Export Inflows (cash crops, gold) | ↑ FX supply, stronger TZS | Lower imported inflation | Enhanced export sector performance |

| Tourism & Transport Receipts | Diversified FX earnings | Supports price stability | Service sector growth stimulus |

| IFEM Liquidity & Lower BoT Intervention | Market-driven stability | Reduces exchange rate pass-through | Business confidence enhancement |

| Strong Reserves (4.8 months import cover) | External buffer | Anchors inflation expectations | Investment climate improvement |

| Energy Price Moderation | Reduced import costs | Energy inflation decline | Lower production costs |

| Monetary Policy Credibility | Exchange rate anchor | Inflation expectation management | Stable planning environment |

The stabilization of the Tanzania Shilling in June 2025 represents a confluence of positive economic fundamentals, including robust seasonal export inflows from gold and agricultural commodities, enhanced foreign exchange market liquidity, and prudent monetary policy management. The Tanzania Shilling has strengthened 6.44% over the past month, and is up by 8.34% over the last 12 months, demonstrating sustained improvement in currency performance.

This currency strength, combined with controlled inflation averaging 3.2-3.3% within the target range, has created a stable macroeconomic environment supporting Tanzania's economic growth trajectory. The reduced need for central bank intervention, strong external reserves, and diversified export base provide a solid foundation for continued currency stability and economic expansion, positioning Tanzania favorably for sustained development and regional economic integration objectives.

| Indicator | June 2025 Value | Previous Period | Change / Context |

| USD/TZS Exchange Rate (avg) | 2,631.56 | 2,698.42 (May 2025) | Strengthened |

| Annual Depreciation Rate | 0.21% | 12.5% (June 2024) | 60-fold improvement |

| USD/TZS Rate (Aug 7, 2025) | 2,470.00 | — | Strengthened 6.44% in past month |

| Gold Export Earnings | USD 3.66 billion | — | Major FX inflow |

| Tourism Receipts | USD 3.83 billion | 2.2 million visitors | Boost to services sector |

| IFEM Turnover | USD 121.50 million | USD 110.8 million (May 2025) | Higher liquidity |

| BoT FX Intervention (Net Sales) | USD 6.3 million | USD 53 million (May 2025) | Large reduction |

| Foreign Exchange Reserves | USD 5.97 billion | — | 4.8 months import cover |

| Headline Inflation | 3.3% | 3.2% (May 2025) | Within 3–5% target |

| Energy Inflation | 2.1% | 6.1% | Decline due to currency strength & oil prices |

Tanzania is experiencing an unprecedented surge in Foreign Direct Investment (FDI), positioning itself as East Africa’s premier investment hub. With a strong policy and infrastructure reform agenda, Tanzania is not only attracting capital but also creating jobs, transferring technology, and reducing poverty in line with its Vision 2050 of achieving a USD 1 trillion economy.

Programs like Vikapu Bomba (training 5,000 women in 2024 and targeting 50,000 by 2030) and SEZs like Kibaha Textile Park (projected 38,400 jobs) emphasize inclusive development. FDI also aligns with SDG 8 (Decent Work) and SDG 13 (Climate Action) by promoting green energy and equitable employment.

Tanzania’s FDI trajectory showcases how robust policy, sectoral strategy, and institutional reform can unlock transformative economic growth. By addressing remaining gaps and promoting equity, Tanzania is on course to become a regional economic powerhouse by 2030.

In October 2024, the Tanzania Shilling showed signs of stabilization, appreciating slightly against the US Dollar after months of depreciation. This shift can be attributed to improved foreign exchange liquidity from key export sectors such as cashew nuts, gold, and tourism, alongside strategic interventions by the Bank of Tanzania. Despite a gradual depreciation trend over the years, recent developments suggest a positive turn in external sector performance and effective exchange rate management.

1. Exchange Rate Movements:

The Tanzania Shilling showed a slight improvement in October 2024, appreciating by 0.28% compared to September 2024. This indicates a stabilization trend after several months of depreciation. The depreciation rate over the past year has decreased, suggesting that external pressures on the currency may be easing.

2. Key Factors Affecting the Exchange Rate:

A. Improved Foreign Exchange Liquidity:

Several key export sectors have contributed to increased foreign exchange inflows, which helped stabilize the Shilling:

B. Bank of Tanzania Intervention:

3. Historical Exchange Rate Data (2017-2023):

A look at historical data reveals a gradual depreciation trend of the Tanzania Shilling over the years, but with some periods of relative stability:

From 2017 to 2023, the Shilling depreciated steadily, with the rate increasing by about TZS 150 per USD over the period. This is consistent with inflationary pressures and a growing trade deficit.

4. Interbank Foreign Exchange Market (IFEM) Activity:

The Interbank Foreign Exchange Market (IFEM) activity shows significant changes in the volume of transactions:

The sharp increase in market activity reflects growing demand and supply for foreign exchange in the market, indicating heightened foreign exchange transactions. This could be tied to the improved liquidity from exports and the increasing demand for USD in the economy.

5. Summary and Key Insights:

6. Conclusion:

The recent appreciation of the Tanzania Shilling and the improved annual depreciation rate suggest that external sector performance is improving. Factors such as strong export performance, particularly in cashew nuts, gold, and tourism, have bolstered foreign exchange liquidity. Additionally, the Bank of Tanzania's careful market interventions have contributed to the exchange rate’s stability, easing pressure on the Shilling.